25 May Acquisition vs. Startup?

Acquisition vs. Startup?

So you either just graduated or will soon be graduating from dental school. You have already made the decision that you do not want to work for someone else. You know that practice ownership is the only way you can achieve the income level you desire. You have also learned that it is possible to obtain financing even if you are weighted down in school debt. But now you are struggling with the quintessential question:

“Should I purchase an existing practice or start a practice from scratch?”

This is quite possibly the most important career decision you will ever be faced with and the choice you make now will most assuredly have a major impact on your entire career. Dental equipment salespeople suggest that a practice start-up is your best option; practice brokers state that a practice acquisition is the best. Your dental school professors may be advising you to take the associate route. Unfortunately, depending on which “expert” you talk with, you are finding that the so-called “informed opinions” vary significantly. Well not to be outdone, let us throw PARAGON’s two cents into the decision making pot.

Regardless of what others may tell you, you will virtually always end up with significantly more income from a practice you acquire than from a practice you start from scratch! In addition, the income will be much more immediate. It is a matter of simple logic. The source of cash flow for any dental practice is a quality patient base. A start-up practice has no patients; an established practice has an abundance of quality patients.

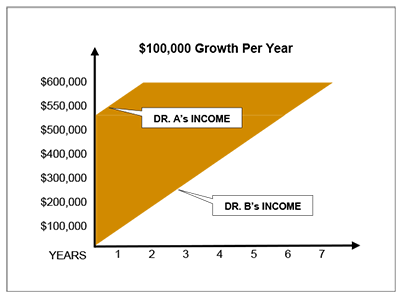

Let’s look at a simple comparison: Dr. A and Dr. B would both like to own a practice with gross production revenues of $700,000 per year. Dr. A and Dr. B each believe that they can achieve an annual production growth rate of $100,000 per year (without having to accept low fee plan or managed care patients into their practices).

Let’s look at a simple comparison: Dr. A and Dr. B would both like to own a practice with gross production revenues of $700,000 per year. Dr. A and Dr. B each believe that they can achieve an annual production growth rate of $100,000 per year (without having to accept low fee plan or managed care patients into their practices).

Dr. A pays $350,000 to acquire a practice that is currently grossing $500,000. Dr. A also borrows an additional $75,000 to cover closing costs and working capital. Dr. B starts a practice from scratch purchasing $175,000 of new equipment, furniture, fixtures and supplies. He also invested an additional $50,000 in leasehold improvements to make sure the leased office space was set up perfectly for how Dr. B wished to work. Dr. A immediately has access to a quality, fee-for-service patient base of 1,500 active patients. Dr. B has an immediate patient base consisting of his family and close friends.

Growing at an annual pace of $100,000 per year, Dr. A quickly reaches his target annual gross revenue goal of $700,000 in just two short years. Of course at $100,000 a year, it takes seven years for Dr. B to reach the exact same $700,000 target gross revenue goal.

Upon the completion of the first 7 years of practice (at which time both practices are equal in size based on annual gross revenues), Dr. A’s practice produced total gross revenues of $4,800,000. Dr. B’s practice produced total gross revenues of $2,800,000.

We can already see that Dr. A will accumulate $2,000,000 more in total practice revenues over the first 7 years, but what about net incomes?

Let’s assume that both practices have an overhead percentage, excluding debt service, of 55%. Please note that this is really not a realistic assumption since the overhead for practices with the lower gross revenues is actually much higher percentage of the total practice revenues. For example, a staff salary of $20,000 is 20% of a $100,000 gross revenue, while that same salary of $20,000 is only 4% of a gross revenue of $500,000. Annual rent of $24,000 is 24% of a gross revenue of $100,000, while that same rent factor is only 4.8% of a $500,000 gross revenue.

Dr. A would enjoy a net revenue, before paying debt service payments, over the 7 year period of $2,160,000 ($4,800,000 less 55% overhead of $2,640,000). Dr. B would enjoy a net revenue over the same period of $1,260,000, or $1,000,000 less than Dr. A.

Let’s also assume that both Dr. A and Dr. B financed their loans at 8% interest with a 7 year payback. Again, this is really not a realistic annual cash flow comparison because the type loan that Dr. B procures will typically have to paid off in 5 to 7 years while Dr. A loan would generally be set up on a 10 year amortization (much lower monthly payments).

Dr. A borrows $425,000 ($350,000 for the practice acquisition and $75,000 working capital). The monthly payments at 8% for 7 years are $6,624.14. Dr. B’s monthly payments on his $225,000 loan at 8% for 7 years is only $3,506.90. So, Dr. A pays $3,117.24 more per month, or $261,848 more over the same 7 year period. However, Dr. A had an extra $1,000,000 in net revenues before debt service, so his true increased financial benefit over Dr. B is $738,152!

A true “apples to apples” comparison, both doctors are free of debt and both practices are exactly the same size in terms of gross revenues! Yes, we agree, Dr. A still has older equipment (but Dr. B’s equipment is now 7 years old so it is not exactly the latest and greatest anymore either). But, Dr. A also has an extra $738,152 (plus compound interest) at his disposal to re-equip his office completely. You tell us which doctor made the best decision!